North Sea Mythbuster: Why the Seven Arguments Against Drilling Are All Wrong

Former trader Francis Holburne explains the holes and fallacies in the most common arguments trotted out by Net Zero zealots

With America’s war in Iran causing extreme fluctuations in global energy prices, the debate around energy extraction in Britain has of late gained a renewed sense of urgency. Why is Britain so vulnerable to these kinds of energy shocks and how can we make our economy more resilient? Daily Sceptic readers hardly need to be told that it is our reckless pursuit of Net Zero that’s principally to blame for this sorry state of affairs. And yet, as such debates rage in the mainstream media, we see Net Zero advocates blithely trot out the same set of unflushable arguments to defend their cause. Sadly, in the less-than-intellectually-rigorous environments of, say, LBC or BBC Question Time, these arguments may even appear convincing on the surface. In reality, each suffers serious flaws. Here are seven of the canards you hear most often – and why they’re wrong.

“Prices are set on international markets so UK extraction doesn’t help consumers”

This is perhaps the most persistent myth in the debate, and the most frequently cited, particularly since the first energy price spikes following the war in Ukraine in 2022. While it is true that benchmark prices for oil and gas exist internationally – Brent and TTF come to mind – there are plenty of dislocations in regional markets for gas. To claim that the existence of global benchmark prices used by traders implies that there is a single international price for oil and gas that must be paid by all consumers is to ignore the realities of market structure.

In fact, the energy crisis brought on by the war in Ukraine is the most instructive counterexample. The removal of Russian gas from European markets led to extreme price dislocations across regions. Massive spreads between US and European gas prices arose, as European countries scrambled to bid for liquefied natural gas (LNG) cargoes. It is precisely the marginal, most volatile source of supply that sets prices during periods of market stress. Commodity trading firms were able to make vast profits exploiting these dislocations. It is in fact their entire business model. Mostly they avoid flat price risk, preferring to trade the price differences of commodities across regions.

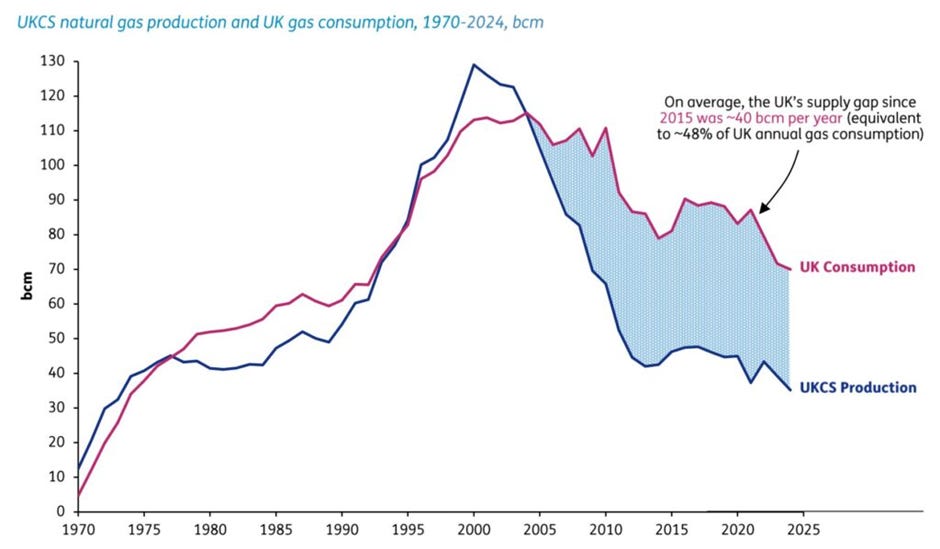

Britain currently imports about half its gas consumption. Domestic production would directly reduce reliance on LNG spot markets. Likewise, it reduces our exposure to geopolitical shocks. In 2022, the Energy Price Guarantee (which compensated suppliers for selling energy below market prices) cost the taxpayer £44 billion in support for households, in addition to the exorbitant prices paid for LNG to meet demand. Finally, higher domestic production improves the country’s current account balance, which in turn supports sterling and reduces inflation. This is a real, albeit indirect benefit to consumers.